Looking over the last six months, as economic conditions start to improve in WA, Quadrant Advisory has seen an increased level of inquiry in the property sector from both clients and prospective clients.

There is a common perception that banks’ risk appetites have tightened and industry participants are aware of other funding alternatives available in the marketplace.

Following their Commercial Real Estate (CRE) sector report in March 2017, APRA issued its latest insight into lending to the CRE sector on 18 December 2018. Some key callouts to see if their observations are consistent with clients’ perceptions are as follows.

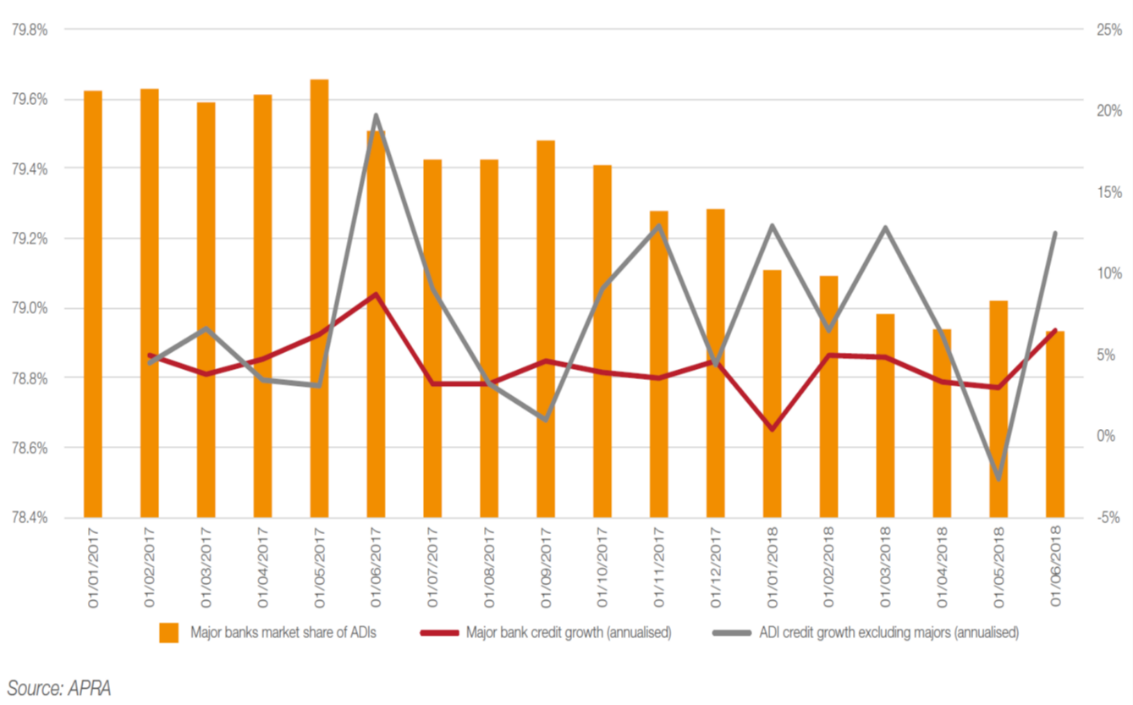

The decline in market share of the Big 4 banks for lending to property across all of its various segments is demonstrated in the graph below. Non-major banks and other funders are increasing their lending to the property sector at the expense of the larger banks.

Source: PricewaterhouseCoopers Banking Matters – August 2018

As a result of some of APRA’s key findings above, a “funding gap” has emerged in the CRE sector and there are now a number of non-bank financiers who have a different risk appetite and are quicker to market than banks. Specialised property funders include MaxCap, Wingate, Qualitas, Chifley Securities and CVS Lane Capital Partners to name but a few.

Given APRA’s ongoing focus on the CRE lending sector, it is likely that industry participants will look to source funding from non-bank providers given their different risk appetite parameters, however at a greater interest rate cost than that provided by banks.

Quadrant Advisory has significant insight, knowledge and experience in dealing with banks and other financiers and can leverage this expertise for your organisation’s benefit. If you require assistance on assessing your credit risk metrics and your ability to source debt funding, please contact Quadrant Advisory’s managing director, Paul O’Farrell.